The Math Behind Cracking Packs

A quant’s look at sealed MTG product pricing, expected value, and why you almost always lose money opening boosters.

The real (math) paper is here: A Valuation Framework for Sealed Products in Collectible Card Markets: Expected Value, No-Arbitrage Pricing, and the Sealed Opened Spread

—

There’s a ritual that every Magic player knows. You walk into the LGS on a Friday night, maybe for draft, maybe just because you were in the neighborhood and the gravitational pull of cardboard is real. You see the booster packs behind the counter. You tell yourself you’re not going to buy one. You buy one.

You hold it for a second. You do the thing where you sort of bend it slightly, as if the flex of the wrapper might reveal whether destiny has placed a $40 mythic inside. It hasn’t, but you crack it anyway.

Commons. Commons. An uncommon you already have four copies of. Then the rare -- and it’s some forgettable 3-mana do-nothing that’s already bulk on TCGPlayer. Four dollars and forty-nine cents, gone. The dopamine cycle resets. You consider buying another one.

I’ve been thinking about this moment a lot, not as a Magic player but as someone who spends his professional life staring at pricing models and probability distributions. Because when you really break it down, a sealed booster pack is a financial instrument. It’s a lottery ticket over a portfolio of assets -- individual cards -- with known probability distributions and observable market prices. And like most lottery tickets, the math is not on your side.

So I built a model. I ran 100,000 simulated pack openings. And I want to walk you through what I found, because some of the numbers are worse than you think, and the reasons why are more interesting than you’d expect.

Two Prices, One Product

Here’s the core idea. Every sealed MTG product lives a double life.

On one hand, it has a market price as a sealed object. A draft booster costs $4.49 at your LGS. A collector booster box goes for $250. A commander precon lists at $50. Call this the sealed value, or V(sealed, t) -- the price at time t, because prices move.

On the other hand, that same product contains cards, and each card has its own price on the secondary market. If you could open the product and instantly sell every card at market price, you’d collect some total amount. The expected total -- averaging over all the possible cards you might open -- is the opened value, V(opened, t).

The difference between these two numbers is what I call the sealed-opened spread:

When the spread is positive, you’re paying more for the sealed product than the cards inside are worth on average. When it’s negative, you have an arbitrage opportunity -- buy sealed, open, sell singles, profit. In theory, anyway.

How to Actually Calculate the EV

A draft booster has about 15 cards, but they’re not all drawn from the same pool. There’s a structure to it -- a slot system -- and this is where the math lives.

That rare/mythic slot at the back of the pack? It draws a rare 7 out of 8 times, and a mythic 1 out of 8. Within each rarity, every card is equally likely. So if a set has R rares and M mythics, the probability of pulling any specific card is:

The three uncommon slots each draw uniformly from the uncommon pool. The ten common slots draw from commons. There’s usually a bonus slot for foils or special treatments.

More generally, each slot k in the product draws a card according to some probability distribution over all Z cards in the set. The expected dollar value of whatever card lands in that slot is:

where pi(k,i) is the probability that card i ends up in slot k, and p(i,t) is that card’s market price at time t. Sum this across all n slots in the product and you get the total expected value of opening:

A useful property here: this formula works regardless of any weird collation rules or no-duplicate constraints between slots. Linearity of expectation doesn’t care about dependencies. The expected value of the sum always equals the sum of the expected values. That’s not an approximation -- it’s a theorem. It always holds.

For a standard draft booster, where slots draw uniformly within rarity classes, this simplifies to something very clean:

where the bar notation means the average price across all cards of that rarity. This is the workhorse equation. Plug in average prices by rarity and you’ve got your EV.

The No-Arbitrage Condition (or: What Finance Theory Says Should Happen)

If you’ve taken a finance class, you know where this is going. In a perfect market -- no transaction costs, perfectly liquid cards, risk-neutral participants, symmetric information -- the sealed price should equal the expected opened value. Exactly. Always.

Why? Standard arbitrage reasoning. If the sealed product costs less than the expected value of its contents, traders buy sealed, crack packs, sell singles, and pocket the difference. They keep doing this until the sealed price gets bid up to match. If the sealed product costs more than expected value, traders should sell sealed and buy equivalent singles... except here’s the catch.

You can’t re-seal a booster. You can’t buy 15 singles and shrink-wrap them into a factory-sealed pack. The arbitrage only works in one direction. You can punish a sealed discount by buying and opening, but you cannot punish a sealed premium because that would require manufacturing sealed product from scratch.

This one-directional arbitrage is the single most important structural feature of the MTG sealed market. It means sealed products can sustain a premium above expected value indefinitely. There’s no mechanism to push the price down.

A sealed booster is, in financial terms, a lottery ticket over a portfolio of assets. Under risk neutrality, the ticket should cost exactly its expected payoff. In practice, it almost never does.

I Simulated 100,000 Pack Openings

Theory is nice. Numbers are better. I built a generic set with realistic parameters: 60 rares, 20 mythics, 80 uncommons, 101 commons. I gave the cards a realistic price distribution -- a couple of chase mythics in the $30-45 range, a handful of playable rares at $5-12, and an enormous pile of bulk worth less than a quarter. This matches what most Standard-legal sets actually look like.

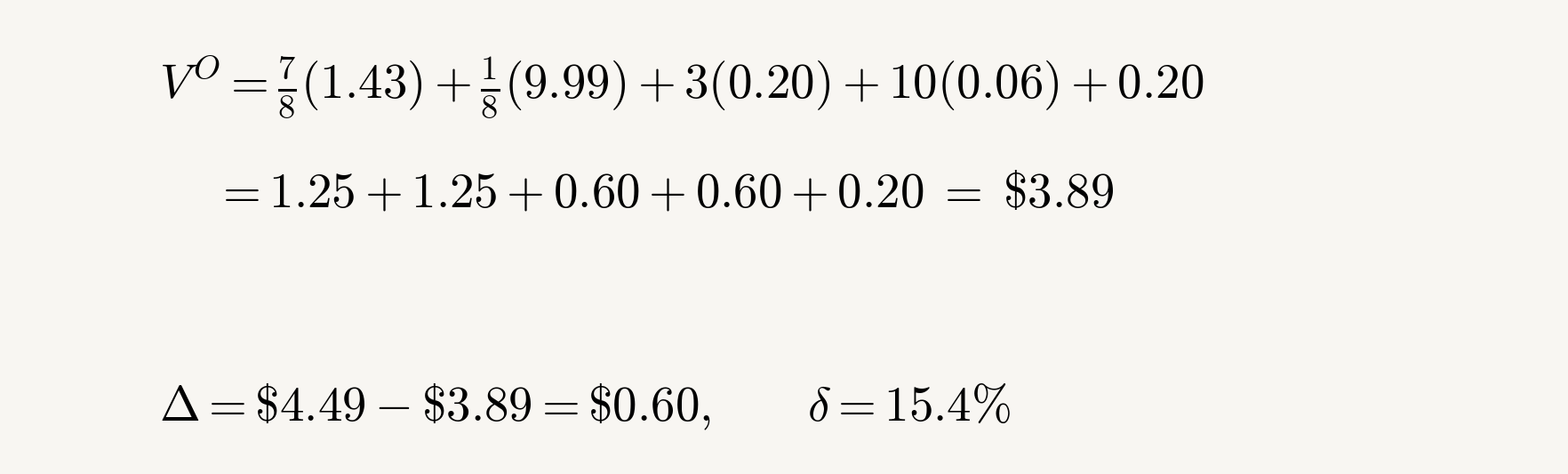

Then I simulated opening 100,000 draft boosters. Each simulation draws cards according to the actual slot probabilities and sums up the market value. Here are the numbers plugged into our formula:

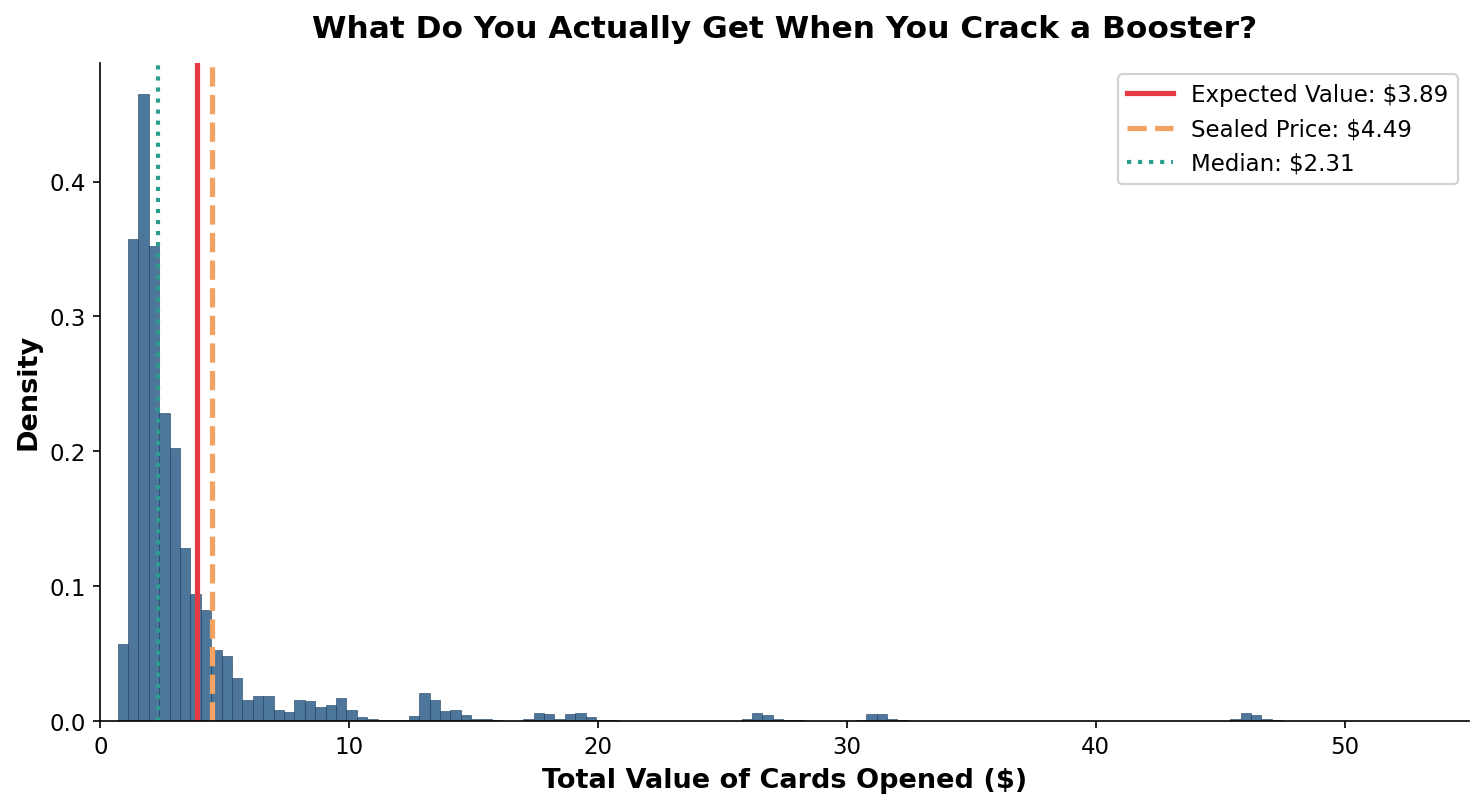

And here’s the full distribution of outcomes across all 100,000 simulated openings:

Take a minute with this chart. It doesn’t look like a bell curve. It looks like a wall on the left side with a long, thin tail stretching to the right. That shape tells the whole story: the overwhelming majority of packs yield very little value, and the average is pulled up by rare big hits.

The numbers:

Expected Value (Mean): $3.89 Median: $2.31 Standard Deviation: $5.35 Sealed Retail Price: $4.49

The median -- $2.31 -- is the number that matters for your lived experience. It’s the outcome you’ll hit more often than not. More than half the time, the cards you rip are worth barely half what you paid for the pack.

The mean ($3.89) is higher, but it’s an illusion of aggregation. It’s being dragged up by the small percentage of packs where you hit a $30+ mythic. Those wins are real, but they’re rare -- and when EV calculators show you “$3.89 expected value,” they’re showing you the mean, not the median. Your typical pack opening is the median. The mean is a mathematical abstraction that averages in outcomes you’ll see once every 50 or 100 packs.

And the standard deviation -- $5.35 -- is larger than the mean itself. The coefficient of variation exceeds 1. This is, by any statistical standard, an extremely high-variance activity. The variance of the total opened value decomposes as:

In practice, the variance is dominated by the rare/mythic slot. The common and uncommon slots contribute near-zero variance because their prices are tightly clustered around bulk value. One slot drives almost all the risk.

Your Actual Odds of Breaking Even

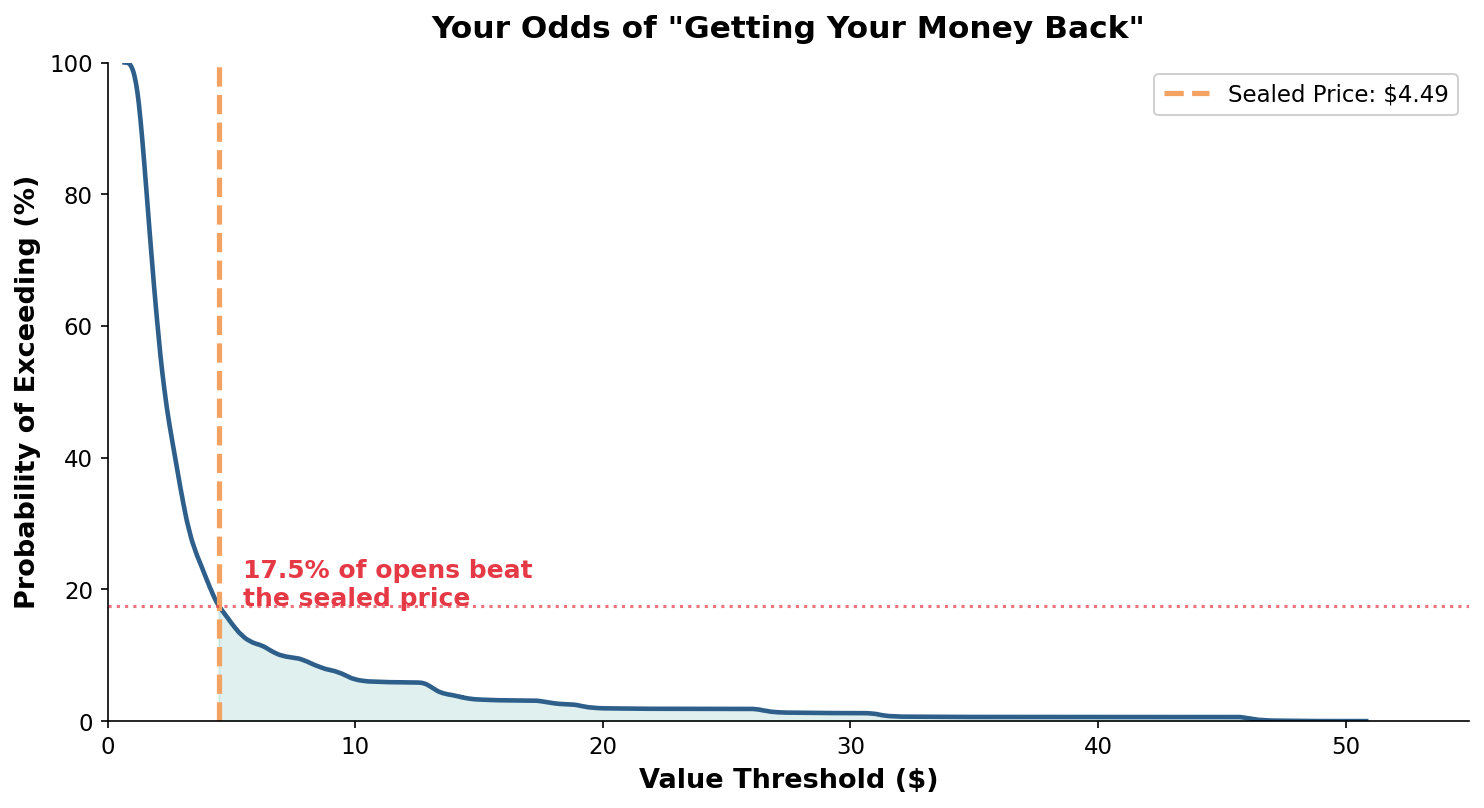

This chart shows the probability that the cards you open exceed any given dollar threshold. Find $4.49 on the x-axis -- the retail price of the booster -- and read across.

Only 17.5% of pack openings beat the sealed price. Roughly 1 in 6. The other five times out of six, you lost money relative to what you paid.

About 6% of packs yield $10 or more. Under 2% clear $20. And nearly 40% of the time, you open less than $2 worth of cards from a $4.49 pack. Forty percent.

These aren’t “bad luck” numbers. This is the mathematical structure of the product. The rarity distribution is designed so that most packs contain mostly low-value cards, with occasional high-value hits keeping the average attractive enough to sustain demand. It’s the exact same mechanism as a slot machine.

Where Does the EV Actually Come From?

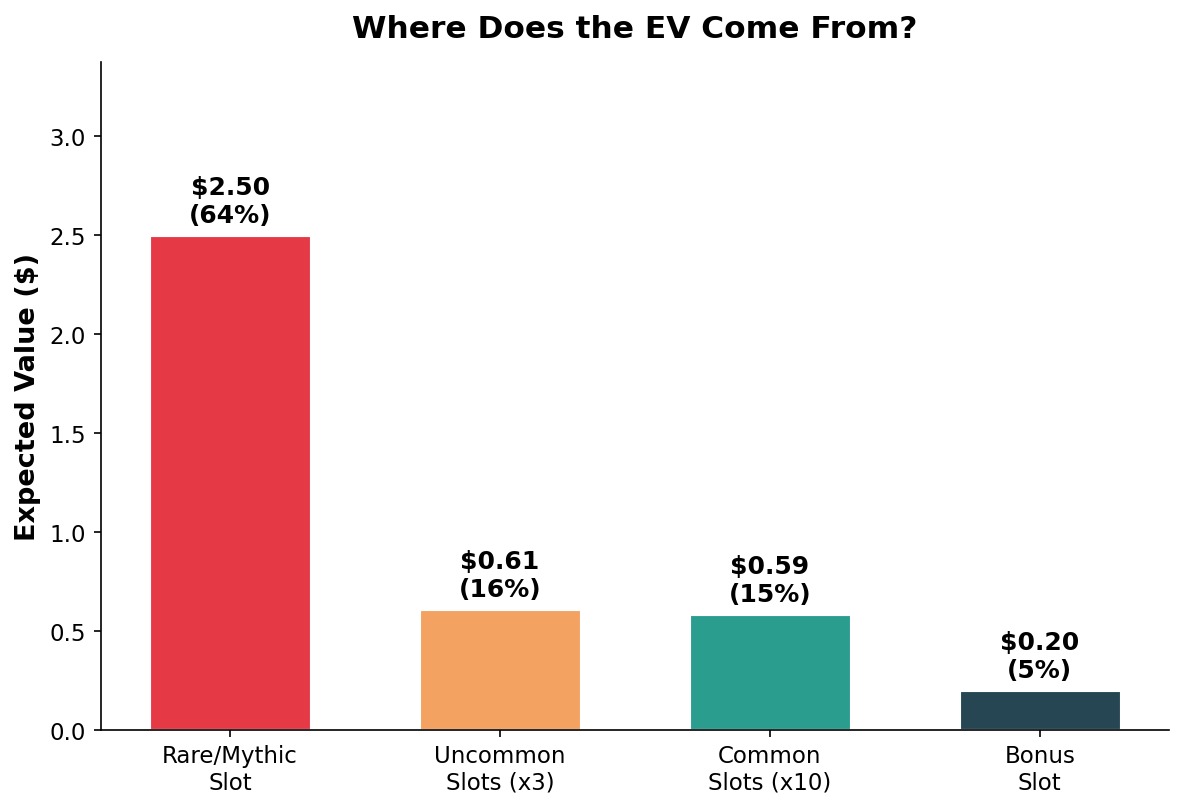

Here’s a breakdown of where the expected value originates, by slot type.

The rare/mythic slot -- one card out of fifteen -- accounts for roughly 64% of the total expected value. One slot. Nearly two-thirds of the value. The ten common slots combined contribute about 15%. The three uncommon slots add roughly 16%. The bonus slot is a rounding error.

This is why opening packs feels so binary. You’re not opening a diversified portfolio of fifteen assets. You’re opening one meaningful lottery draw surrounded by fourteen pieces of near-worthless filler. The pack is basically worth whatever the rare is worth, plus noise.

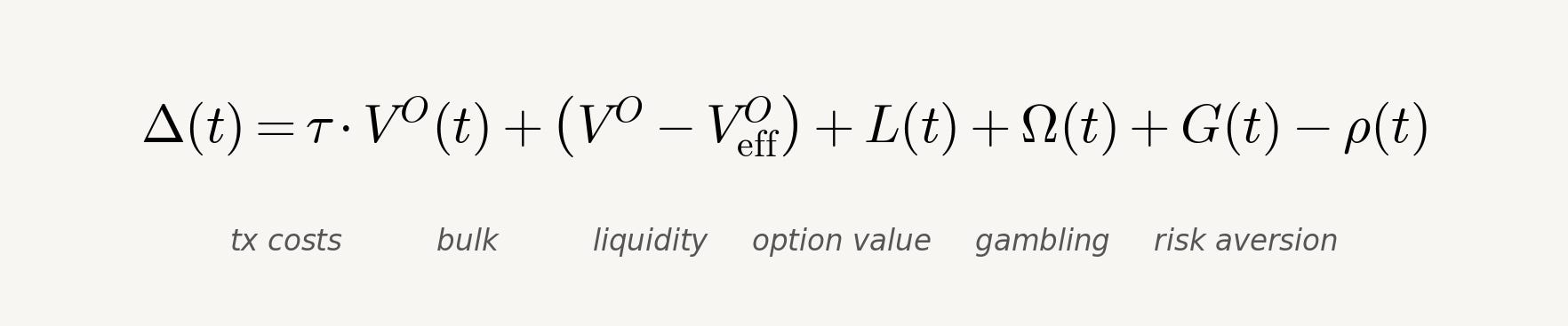

Why You Pay More Than EV (And Why That’s Rational)

So the EV is $3.89 and the sealed price is $4.49. That’s a gap of about $0.60, or roughly 15% above expected opened value. Where does this gap -- this “sealed premium” -- come from?

Transaction costs are the biggest piece. If you actually tried to sell every card you open on TCGPlayer, you’d lose 10-13% to platform fees, plus shipping, plus the time you spend photographing, listing, packaging, and mailing. A $4 rare nets you maybe $3.40 after fees. Applied across the board, transaction costs alone justify a 12-15% sealed premium. Formally, if the proportional transaction cost is tau, the net expected value of opening becomes:

So the relative spread should at minimum equal the transaction cost rate. If tau is 12%, the sealed product should trade at least 12% above EV just to cover fees.

Most of your cards are literally unsellable. A common worth $0.05 costs more to ship than it’s worth. Nobody is listing bulk commons on TCGPlayer. If you filter the expected value calculation to only include cards worth more than some minimum threshold -- the ones you’d actually bother selling -- the “effective EV” drops well below the theoretical number:

The indicator function zeroes out every card below the minimum sellable price. Once you exclude everything below $0.25, probably half the cards in your pack contribute zero realizable value.

Irreversibility creates option value. Once you open a pack, it’s open forever. But a sealed pack preserves the option to open it later, when card prices might be different. Maybe a card gets unbanned and spikes. Maybe the set goes out of print and sealed supply dries up. Keeping the product sealed preserves this optionality. Opening it destroys the option. This is directly analogous to the time value of an American option in finance -- early exercise (opening) sacrifices future flexibility.

People enjoy the variance. This is the behavioral finance angle, and it’s real. Lottery tickets trade above expected value everywhere in the world because people derive utility from the act of gambling itself. The thrill of peeling back the wrapper and seeing a chase mythic has positive value. MTG players know the math is against them. They buy packs anyway. That willingness to pay above EV for the experience is the gambling premium, and it’s baked into sealed prices.

Putting it all together, the spread decomposes into identifiable components:

The sign of the spread depends on the relative magnitude of these forces. For in-print products, transaction costs and bulk dominate, and the spread is positive (sealed premium). For out-of-print products with high-value singles, the spread can turn negative, making it profitable to buy sealed and crack.

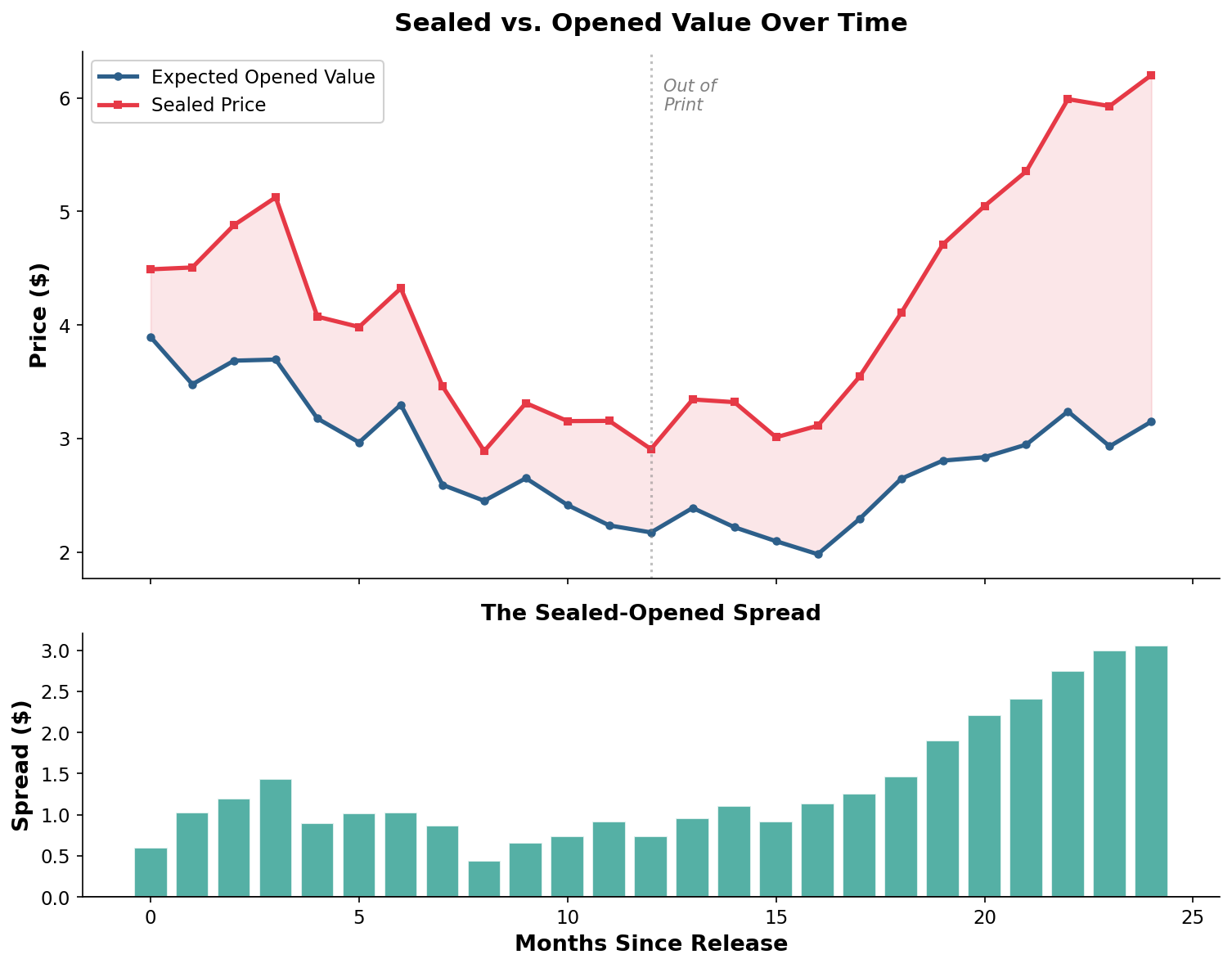

How Prices Evolve Over Time

Both the sealed price and the opened EV move over time, but they don’t move in lockstep.

In the early months after release, while the set is still in print, the sealed price tracks the opened EV with a fairly stable premium -- the transaction cost wedge I described above. If a card spikes because it wins a Pro Tour, the EV jumps and sealed prices follow with a short lag. If the set gets “opened out” and singles prices collapse from oversupply, sealed prices usually hold up a bit better, widening the spread.

The interesting dynamics start when a set goes out of print. Sealed supply becomes fixed. Every box that gets opened or sits in someone’s closet reduces the available float. If the set’s singles retain value -- playable cards in Modern, Legacy, or Commander -- the sealed premium starts compounding. Collector demand for unopened product kicks in. The sealed-opened spread widens monotonically.

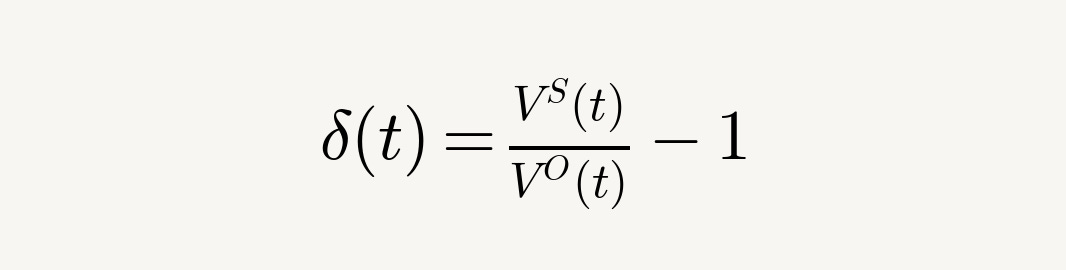

A useful way to track this over time is the relative spread:

For in-print product, delta(t) hovers around 10-40%. For out-of-print iconic sets, it can exceed 200-300% as the sealed object becomes a collectible in its own right.

For truly iconic sets -- the ones with lasting demand -- this process can run for years. A sealed booster box from the mid-1990s trades at thousands of dollars, far exceeding the expected value of the cards inside, because the sealed object itself has become a collectible. The option value dominates everything else.

For forgettable sets where singles crater, the opposite can happen: sealed prices drop below the depressed EV, creating genuine windows where buying sealed and cracking for singles is profitable. These windows exist. They don’t last long, because they’re the one form of arbitrage that actually works -- the downward kind.

The Framework Generalizes

Everything I’ve described applies to draft boosters, but the math works for any sealed MTG product. You just change two parameters: the number of card slots n and the probability distributions per slot.

Collector Boosters have roughly 15 cards but every slot is rare-or-higher rarity. Higher EV per pack, much higher variance, much higher sealed price. Same framework, amplified dynamics.

Commander Precons contain 100 cards with fully deterministic contents -- no randomness at all. The opened value is just the sum of 100 known card prices. The spread reflects pure transaction costs and the convenience of buying a pre-assembled deck versus sourcing 100 singles.

Booster Boxes contain 36 draft boosters (or 12 collector boosters). EV scales linearly -- 36 times the single booster EV. But variance per dollar spent is reduced by the diversification of opening many packs. Box-level collation (you’re roughly guaranteed one of each rare) smooths things further. The box is a less volatile bet than the individual pack.

Is the MTG Market Efficient?

Semi-efficient, at best.

High-demand, high-liquidity cards on major platforms are priced competitively. Your Sheoldreds, your fetch lands, your format staples -- these have tight bid-ask spreads and fast turnover. The market does a reasonable job pricing these.

But the long tail is messy. Niche foils, foreign-language printings, obscure commander staples, special treatments -- these have thin markets, wide spreads, and persistent mispricings. The sealed market is even less efficient: retail prices are sticky, distributor markups introduce multi-tier pricing, and collector demand adds pricing factors that have nothing to do with card-level fundamentals.

The no-arbitrage condition is best understood as a theoretical anchor -- the price the market should gravitate toward if frictions didn’t exist. The real-world equilibrium is a friction-adjusted version: sealed price equals EV minus transaction costs, plus option value, plus gambling premium, minus risk discount. Each of those terms shifts over time, across products, and across sets. The spread is never truly “correct” -- it’s just the current market’s best guess at balancing those forces.

So What?

Opening boosters is a negative expected value proposition at retail. It always has been. The sealed premium exists for real, defensible, economically rational reasons -- transaction costs, unsellable bulk, option value, and the entertainment premium built into the act of gambling.

The median outcome -- the experience you’ll have more often than not -- is dramatically worse than the mean that EV calculators show you. When someone says “this pack has $3.89 of EV,” they’re technically correct but practically misleading. Your typical pack opening yields $2.31. The $3.89 is a phantom average pulled up by low-probability jackpots.

None of this means you shouldn’t crack packs. Cracking packs is fun. That fun has real, quantifiable economic value -- it’s why people pay above EV for lottery tickets worldwide. Just be honest about what you’re buying: the experience, the dopamine, the communal moment of ripping a pack at FNM and slamming a chase mythic on the table while your friends lose their minds. That’s worth something real.

But if you’re approaching MTG product as a financial proposition -- as an investment or a speculation -- the math says something different. Buy sealed. Don’t open it. Let declining supply and option value do the work. The sealed premium is the trade. The pack cracking is the entertainment line item.

Methodology: Monte Carlo simulation of 100,000 booster pack openings using a generic set with 60 rares, 20 mythics, 80 uncommons, and 101 commons. Card prices drawn from realistic skewed distributions calibrated to resemble a typical Standard-legal set. Full mathematical treatment available in the companion paper. All models are simplifications -- actual results depend on the specific set, current market prices, and your platform’s fee structure.